SBA 504 Loan Timeline Breakdown: Where Most Delays Actually Happen

SBA 504 Loan Timeline Breakdown: Where Most Delays Actually Happen

Have you ever wondered why your SBA 504 loan is taking weeks or months longer than you planned?

You are not alone. The SBA approved over 85,000 SBA loans in fiscal year 2025, totaling $45 billion in loan volume. Yet for thousands of those borrowers, the process stretched far beyond the expected window, not because of the SBA, but because of predictable, avoidable gaps nobody warned them about.

The average SBA 504 loan timeline runs 60 to 90 days. In complex cases, it reaches six months. Every unnecessary week costs your business real money. This breakdown tells you exactly where delays happen and what you can do right now to prevent them.

Why the SBA 504 Loan Process Takes Longer Than You Think

The SBA 504 loan involves three parties: the bank covering 50% of the project, the Certified Development Company (CDC) covering 40%, and you putting in as little as 10% as a down payment. Three parties means three separate approval gates and any one of them falling behind stalls everyone else.

The maximum 504 debenture is $5.5 million, with eligibility requiring a tangible net worth under $20 million and average net income under $6.5 million after taxes. That structure gives you long-term fixed rates but it also means three places where your deal can slow down.

The Real SBA 504 Loan Delays — Stage by Stage

When small business owners ask how long does an SBA 504 loan take, the honest answer is: it depends on which stage slows down and why.

Not every stage of the SBA 504 loan process steps carries equal risk. Some stages move quickly when handled well. Others, regardless of how prepared you feel, have built-in variables that catch borrowers off guard. What follows is not a general overview.

These are the five specific points in the SBA 504 loan timeline where deals slow down most often, why they happen, and what you can do at each stage to keep your closing on track.

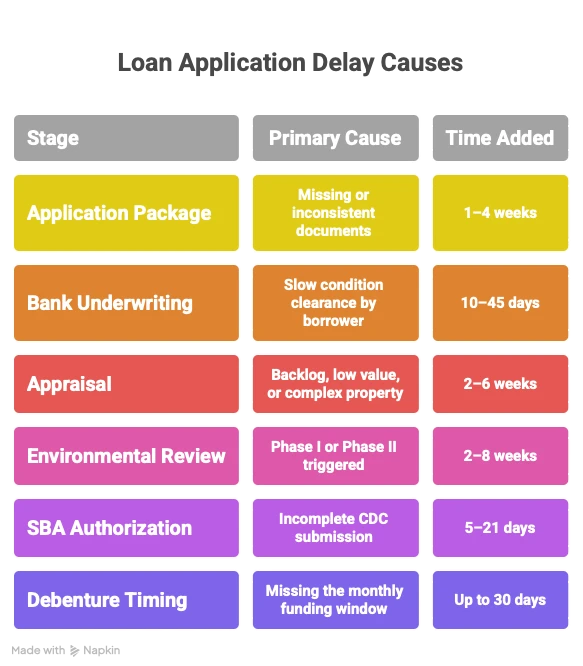

Delay #1: Incomplete Application Package (Adds 1–4 Weeks)

This is where most borrower-caused delays begin. The formal application requires three years of business and personal tax returns, financial statements, a business debt schedule, entity documents, and a signed purchase contract, at minimum.

When documents are missing, outdated, or inconsistent with IRS filings, everything stops. Industry data shows incomplete documentation can double or triple processing time. A clean, complete submission from day one is your most powerful tool.

Pro Tip: Use the SBA 504 Loan Application Checklist to organize every required document before your first submission. Do not wait until you are asked.

Delay #2: Bank Underwriting — Conditions That Pile up (Adds 10–45 Days)

Once submitted, the bank begins underwriting. For non-real estate projects, this takes 10–14 business days. For real estate transactions, it can run up to 45 days.

The delay is rarely the bank working slowly. It is borrowers taking days, sometimes weeks, to clear conditions. When the bank asks for updated financials or a corrected document, every day you take responding adds directly to the timeline.

Quick Fact: Experienced SBA 504 lenders with established bank relationships often resolve conditions faster because both sides already know what the other needs.

Delay #3: The Appraisal — The Most Underestimated Stage (Adds 2–6 Weeks)

For any real estate transaction, a compliant independent appraisal is required by the SBA and it cannot be shared with or borrowed from the bank. The SBA requires its own separate appraisal meeting specific standards under SOP 50 10, as stated in SBA appraisal policy guidelines.

The SBA 504 appraisal timeline ranges from two to six weeks, depending on appraiser availability, property type, and whether the value comes in below the purchase price. Special-purpose properties, medical offices, hotels, gas stations, require more complex methodology and take longer.

If the appraisal flags an environmental concern, a Phase I Environmental Site Assessment is triggered. If that finds a recognized environmental condition, a Phase II investigation follows, adding two to eight more weeks to the SBA 504 closing process.

Tip: Order the appraisal the same day you submit your formal application. Waiting until underwriting completes costs you weeks you cannot get back.

Delay #4: SBA Authorization — Where CDC Experience Matters (5–21 Days)

After the CDC packages your full loan file, it goes to the SBA for authorization. CDCs operating under the Accredited Lenders Program (ALP) have delegated authority, reducing this step to 5–10 business days. Non-ALP submissions go through full SBA review taking 10 to 21 days or more.

An incomplete submission to the SBA resets the clock. This is why choosing experienced SBA CDC 504 loan partners who know exactly what the SBA needs in the package is not a preference, it is critical to your timeline.

Delay #5: Debenture Timing — The 30-Day Trap Nobody Mentions

The SBA 504 closing process actually has two closings. The bank closes first, you take ownership, pay your 10% down, and the bank funds the full interim loan. The CDC closing follows 30–60 days later, once the SBA sells its debenture on a fixed monthly cycle.

The SBA publishes its 504 debenture funding schedule annually. Miss the monthly cutoff date and your final SBA disbursement automatically shifts to the following cycle, adding up to 30 days with no workaround. An experienced CDC plans your closing date around this calendar from the start.

Key Takeaways

- The SBA 504 loan timeline averages 60–90 days but can reach six months for complex deals.

- Incomplete documents are the most controllable delay — prepare your full package before you apply.

- The SBA 504 appraisal timeline is the most underestimated stage — order it the same day you submit.

- Environmental reviews can add two to eight weeks with no way to rush them.

- ALP-certified CDCs process SBA authorization in 5–10 days versus 10–21 for standard submissions.

- The debenture cycle is fixed monthly — missing it adds up to 30 days automatically.

Conclusion

Most SBA 504 loan delays follow a predictable pattern and most are preventable when you work with lenders who know the process at every stage. Document gaps, appraisal timing, environmental reviews, and the debenture calendar are not surprises. They are known variables that experienced teams manage from day one.

504 Capital Corporation is proud to offer its services in Virginia, North Carolina, and Maryland. As the #1 CDC in SBA's Virginia District and an Accredited Lenders Program participant, 504 Capital knows exactly where deals slow down and how to keep yours on schedule from the first call to the final closing.

Contact 504 Capital Corporation today, our team will walk you through every stage, prepare your file correctly from the start, and keep your SBA CDC 504 loan moving.

Frequently Asked Questions

1. Can the appraisal and bank underwriting happen at the same time to save weeks?

Yes and a good CDC coordinates them simultaneously. Running the SBA 504 appraisal timeline parallel to underwriting rather than sequentially is one of the most effective ways to compress the overall SBA 504 loan timeline without skipping required steps.

2. What happens when the appraisal value comes in below the purchase price?

The SBA bases the loan on the lower appraised value. You will need to either renegotiate the purchase price with the seller, increase your down payment, or bring additional equity to close the gap before the SBA 504 closing process can move forward.

3. How does an ALP-certified CDC speed up the SBA 504 loan process?

CDCs in the Accredited Lenders Program have delegated SBA authority, cutting the federal authorization stage from 10–21 days down to 5–10 days. For borrowers with tight timelines, working with an ALP-certified SBA CDC 504 loan provider directly reduces weeks from the process.

4. What documents cause the most application delays?

Inconsistent tax returns, where business financials do not match, IRS filings are the top cause. Outdated financial statements and missing entity documents are close behind. A complete first submission is the single best thing you can do to keep the SBA 504 loan process on track.

5. Does a startup business face a longer SBA 504 loan timeline?

Yes, generally. Newer businesses typically must inject 15–20% equity instead of the standard 10%. More scrutiny on financial projections also extends underwriting. Experienced SBA 504 lenders help newer businesses prepare a stronger package upfront to limit added time.

0 comments

Log in to leave a comment.

Be the first to comment.